Environmental Change is Undermining Sovereign Credit

Finance Must Catch Up

The impact of environmental change on global finance is no longer a theoretical risk—it is a measurable, material threat. As Justin Johnson argues in his Nature Ecology & Evolution comment, mainstream finance has finally begun to incorporate climate risk into risk assessments. Unfortunately, the same cannot be said about nature loss, either amongst practitioners or within academia. Almost a year ago, Matthew Agarwala, in his World View comment for Nature, called on business schools to bring and acknowledge mainstream scientific evidence into training and publishing beyond what is deemed appropriate by the business schools’ rankings. However, these journals continue to lag behind the scientific evidence on nature loss, climate change, and infectious diseases.

Our work published in Nature Ecology & Evolution begins to close this gap. Using forward-looking ecosystem collapse scenarios and knowledge of one of the biggest credit rating agencies, S&P, we derive an artificial intelligence (AI) model simulating sovereign credit ratings of 23 nations.

Our methodological approach relies on linking ecological models from Johnson et al. (2023) on wild pollination, marine fishery collapse, and tropical timber productivity, which are passed through the GTAP-InVEST model and translated into GDP and GDP growth measures through their effects on income, production and trade. We then take these results and plug them into an AI model designed to imitate sovereign credit ratings as closely as possible, providing us with forward looking credit ratings, probabilities of default and borrowing costs.

Extension of Climate Adjusted Ratings

This design extends our previous work published in Management Science in 2023, which was recognised with a Financial Times Responsible Business Education Award. The study presented the world’s first environmentally adjusted sovereign credit rating framework.

Our team, which brought together researchers from Edinburgh Business School Heriot-Watt, University of Sussex Business School, Sheffield University Management School, Cambridge University, and SOAS, used AI to combine IPCC climate models with real world financial indicators. The result was a set of evidence-based, decision-ready assessments of how environmental changes will affect the cost of sovereign and corporate borrowing of over 100 countries.

Sovereign credit ratings, long central to investment decision-making, are used by financial institutions to assess a country’s ability to repay debt. Yet until recently, these ratings largely failed to account for climate change. Our research shows that without substantial emissions reductions, 63 nations could expect a drop in their credit ratings in the next decade.

Germany, India, Sweden, and the Netherlands would each fall by three notches, while the US and Canada would fall by two and the UK by one. By comparison, the economic turmoil caused by the Covid-19 pandemic resulted in 48 sovereign downgrades by the three major agencies.

The study suggests that adherence to the Paris Climate Agreement, with warming limited to below two degrees Celsius, would have little short term impact on sovereign credit ratings while keeping long term effects to a minimum. Without serious emissions reductions, however, 80 sovereign nations would face an average downgrade of 2.48 notches by the end of the century.

India and Canada, among others, could fall by more than five notches, while China could decline by as many as eight. Additional interest payments on sovereign debt arising from the climate induced downgrades alone – a small fraction of the broader economic consequences of unchecked emissions—could cost governments between US$137 billion and US$205 billion.

At stake is one of the world’s largest asset classes: sovereign debt, valued at more than US$100 trillion. It is through sovereign debt markets that governments finance infrastructure, public services, pandemic recovery, and the transition to net zero. As environmental degradation intensifies, so too does the financial pressure on countries most exposed to climate risks.

Nature Adjusted Ratings Are Even Starker

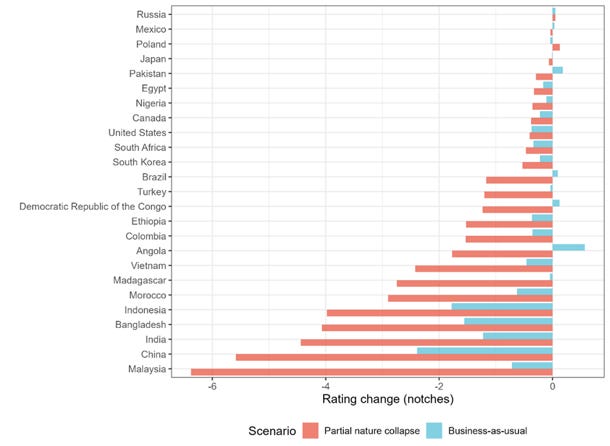

The results of our nature adjusted ratings, released today in Nature Ecology & Evolution, are no more optimistic.

Under a partial collapse scenario, Indonesia, Bangladesh, India, China, and Malaysia could all face downgrades of between four and six notches up to 2030 alone. This translates into approximately US$70 billion and US$49 billion in additional annual debt servicing costs for China and India respectively.

Across the sample, additional annual debt servicing costs are estimated at US$162 billion. This is equivalent to nearly three quarters of global overseas development assistance and would leave many nations at increased risk of sovereign default. For example, Madagascar and the Democratic Republic of the Congo could see their probabilities of default rise by at least 30% once nature related risks are taken into account.

If these additional borrowing costs were financed through higher taxation, they would absorb approximately 1.8% of after-tax income for the median Indonesian citizen, rising to 2.3% in Malaysia and 2.5% in India.

Compared with the UN Global Biodiversity Framework’s target of mobilising US$200 billion annually across 196 countries, our study adds to a growing body of evidence that the costs of protecting nature are substantially lower than the costs of losing it.

For this reason, we call on regulators, central banks, and credit rating agencies to incorporate nature related and climate related risks into mainstream financial risk assessments.

Did We Make A Difference? What More Can Be Done?

Our framework of climate adjusted ratings has already been adopted by global financial institutions. Standard Chartered Bank integrated our findings into its internal models for stress testing and loan provisioning. In a statement of support, the bank described the research as a “game-changer,” noting that it “helped establish a framework on how to assess climate impacts on sovereigns.”

Crucially, this work is influencing not only commercial practice but also public policy. Our research was cited in the Biden-Harris Administration’s National Strategy for Developing Natural Capital Accounts and in the 2023 Economic Report of the President. It also formed the basis for two years of commissioned research by the Inter-American Development Bank, helping to guide sovereign risk assessments in climate vulnerable Caribbean nations.

The growing reach of this research reflects its ability to make environmental science relevant and applicable for financial decision-makers. However, much more work is needed.

Financial markets require credible and accessible evidence on how environmental change translates into material financial risks. Yet current incentives within many business schools continue to favour publication in traditional disciplinary journals, while funding for interdisciplinary research remains limited. At the same time, funding is often directed towards organisations that are not subject to the same standards of methodological scrutiny and peer review as academic research.

As a result, the production of robust evidence needed to support the transition to net zero and nature positive economies remains below what is required.

What we are proposing is not merely an academic exercise. It is a necessary evolution in how researchers, policymakers, regulators, and financial markets understand risk in a world facing accelerating environmental disruption. Scientific evidence, financial practice, and public policy must keep pace with environmental change, or risk being blindsided by its economic consequences.

Figure 1. Credit rating changes under current trends and partial-collapse scenarios